In-Kind Contributions to Registered Accounts and Your ACB

Contributing securities in-kind to a TFSA, RRSP, or FHSA in Canada triggers a deemed disposition under CRA rules. Here's what that means for your ACB and taxes.

If you’ve ever moved investments directly from a margin or cash account into a registered account without selling them first, you’ve made an in-kind contribution. It’s a convenient way to top up a TFSA, RRSP, or FHSA, but the tax treatment is not what most people expect.

What Is an In-Kind Contribution?

An in-kind contribution is when you transfer assets exactly as-is, without liquidating them first. In the context of investing, that means moving securities directly from one account to another rather than selling, moving cash, and repurchasing.

This article focuses specifically on the case where the destination is a registered account. When you contribute securities in-kind to a TFSA, RRSP, or FHSA, the CRA does not treat this any differently from a sale. From a tax perspective, it’s as if you sold the shares at fair market value (FMV) on the date of the transfer, deposited the cash proceeds, and repurchased the shares inside the registered account.

The Deemed Disposition Rule

The CRA’s guidance on TFSA contributions states that in-kind contributions are “considered disposed of at fair market value at the time of the contribution.” The same deemed disposition principle applies to in-kind contributions to RRSPs and FHSAs.

This means:

- If the FMV is greater than your ACB, you have a capital gain and must report it

- If the FMV is less than your ACB, the capital loss is denied and cannot be claimed

Under paragraph 40(2)(g)(iv) of the Income Tax Act, a loss from the disposition of property to a trust governed by a TFSA, RRSP, FHSA, or similar registered account is deemed to be nil. You permanently lose that loss.

This is different from a regular superficial loss, where the denied amount is added to the ACB of the repurchased shares, deferring it to a future sale. Here, the repurchase occurs inside a registered account where ACB has no tax meaning, so the denied loss has nowhere to go and is gone for good.

How the Rules Differ by Account Type

The core deemed disposition rule is the same across registered accounts, but the tax implications of the contribution itself vary.

| Account | Capital gain on deemed sale? | Capital loss claimable? | Contribution deduction? |

|---|---|---|---|

| TFSA | Yes, taxable | No, denied | No |

| RRSP | Yes, taxable | No, denied | Yes, FMV deductible (subject to room) |

| FHSA | Yes, taxable | No, denied | Yes, FMV deductible (subject to room) |

In all cases, the FMV on the date of transfer counts against your contribution room for that account.

One important note on RRSPs: the deemed capital gain on the transfer is reported separately from your RRSP deduction. You may owe tax on the gain even while also receiving a deduction for the contribution.

The T5008 Slip

Your broker should issue you a T5008 slip (Statement of Securities Transactions) early in the following year. This slip reports the deemed proceeds of disposition and your book cost as recorded by the broker. You use this to complete Schedule 3 when filing your taxes, the same way you would for any other sale.

Do not ignore this slip. Even though no cash changed hands, the CRA expects the capital gain to be reported.

One caveat: the book cost on your T5008 may not match your actual ACB if your cost base has been adjusted for events like return of capital distributions or reinvested capital gains. Your own ACB records should take precedence over the broker’s book value when calculating your gain or loss.

What About Registered-to-Registered Transfers?

The deemed disposition rules in this article apply only when securities move from a non-registered account into a registered account. If you are transferring securities between two registered accounts of the same type (for example, moving an RRSP from one institution to another as a direct transfer), there is no deemed disposition and nothing to record for ACB purposes.

Transfers between different registered account types (such as an RRSP to a TFSA) have their own distinct rules and can trigger serious tax consequences. That scenario is outside the scope of this article.

How to Record This in MyACB

Since registered accounts are sheltered from tax, you do not track ACB inside them. What you do need to record is the deemed sale in your non-registered account.

For each in-kind transfer, add a Sell transaction in your portfolio with:

- Date: the date of the transfer

- Quantity: the number of shares transferred

- Price: the FMV (market price) of the security on that date

No corresponding buy entry is needed on the registered account side.

If the transfer resulted in a gain, that’s all you need to do. The capital gain will appear on the transaction and should be reported on Schedule 3.

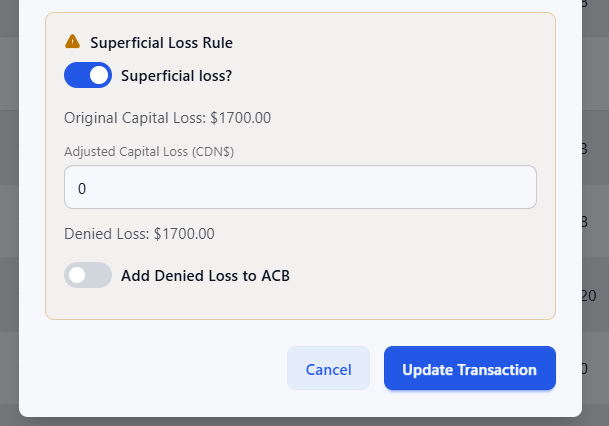

If the transfer resulted in a loss, one more step is required. Edit the Sell transaction and:

- Check Apply Superficial Loss Rule

- Set Adjusted Capital Loss to $0.00. The loss is fully denied.

- Leave Add Denied Loss to ACB unchecked. This is a permanent denial, not a deferral. The repurchase occurred inside a registered account where ACB has no meaning, so there is no ACB to adjust.

A Note on Broker CSV Imports

Your broker may label this transaction in ways that don’t make it obvious. Questrade, for example, records in-kind contributions as a transaction type of “CON” (contribution) with a transaction code of “Withdrawal” on the non-registered account side, since the shares are leaving that account. Other platforms may use “Transfer” or similar labels.

If you import transactions from a broker CSV and the in-kind contribution does not come through as a sale, add the Sell transaction manually. Do not skip it because the broker labelled it as a withdrawal. The CRA classification is what matters, not the broker’s transaction description.

Worked Example

Suppose you hold 100 shares of Shopify (SHOP) in your margin account with an ACB of $95.00 per share. On March 1, SHOP is trading at $112.00 and you transfer all 100 shares in-kind to your TFSA. The calculation is identical for an RRSP or FHSA.

Scenario A: Gain

| Proceeds (100 × $112.00) | $11,200.00 |

| ACB (100 × $95.00) | $9,500.00 |

| Capital gain | $1,700.00 |

You report $1,700.00 as a capital gain on Schedule 3. Your contribution room is reduced by $11,200.00.

Scenario B: Loss (denied)

Now suppose SHOP had dropped to $78.00 instead:

| Proceeds (100 × $78.00) | $7,800.00 |

| ACB (100 × $95.00) | $9,500.00 |

| Capital loss (denied) | $1,700.00 |

You still must record the Sell transaction at $78.00 to clear the shares from your non-registered portfolio, but there is no tax benefit from the loss. Your contribution room is reduced by $7,800.00.

Transfers to a Spouse’s Account

If you transferred shares from your margin account into your spouse’s registered account, the same rules apply. You held the shares in your non-registered account, so the deemed disposition is reported on your tax return, not your spouse’s.

Make sure you and your spouse are using separate portfolios in MyACB. ACB cannot be shared or pooled between spouses. Each person’s holdings must be tracked independently.

Common Mistakes

- Not recording the deemed sale: If you only look at the registered account and see the shares arrived, you might forget the non-registered account side. The Sell transaction is required.

- Expecting to claim a loss: Many investors assume they can harvest a loss by transferring underwater positions to a registered account. The CRA explicitly denies this.

- Using the wrong price: Use the FMV on the date of transfer, not the price you originally paid or the price the following day.

- Treating a broker label as the tax classification: A “withdrawal” or “transfer” label in your broker’s system does not change the tax treatment. In-kind contributions are deemed dispositions regardless of how your broker codes the transaction.

- Mixing spousal portfolios: Tracking a spouse’s holdings in your own portfolio will produce incorrect ACB calculations for both of you.

Frequently Asked Questions

Does this apply to all registered accounts?

Yes, the deemed disposition rule applies to in-kind contributions to TFSAs, RRSPs, FHSAs, and other registered accounts. The tax consequence of the contribution deduction differs by account type, but the deemed sale at FMV is consistent across all of them.

What FMV should I use?

Use the closing market price of the security on the date of the transfer. For ETFs and stocks listed on a stock exchange, this is straightforward. Check your broker’s trade confirmation or end-of-day statement for that date if you’re unsure.

My broker shows this as a “withdrawal” in my non-registered account. Is that right?

Yes. From the non-registered account’s perspective, the shares are leaving, so it appears as a withdrawal or transfer. The tax treatment is still a deemed disposition. How your broker labels the transaction has no bearing on how the CRA classifies it.

Do I need to report this if there’s no gain?

If you realize a capital gain, it must be reported. If you realize a capital loss, it is denied and does not need to be reported as a loss, but you should still record the Sell in MyACB so your share count and cost base stay accurate.

Can I transfer from a registered account back to my non-registered account in-kind?

A withdrawal from a registered account generally establishes a new ACB for those shares in your non-registered account at the FMV on the date of withdrawal (for TFSAs) or at the fair market value as income (for RRSPs). The rules vary by account type. Consult a tax professional for your specific situation.

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax rules can change and individual circumstances vary. Consult a qualified tax professional for advice specific to your situation.

0 Comments

Log in to join the discussion.

No comments yet. Be the first to comment!